OpenAI is no longer just a model lab. It is building a product machine

OpenAI’s agreement to acquire Statsig for about $1.1 billion in stock is not just another tuck-in. It formalises an “Applications” division with its own leadership spine and makes clear where the next phase of competition will be fought: rapid product iteration at consumer and enterprise scale. Statsig’s founder, Vijaye Raji, will become OpenAI’s CTO of Applications, reporting to Fidji Simo, who now leads the Applications group. (sources: Reuters, OpenAI, The Verge)

Why Statsig matters

Statsig is an infrastructure for product velocity, encompassing feature flags, experiment design, telemetry, and decisioning. Folding this into OpenAI places A/B testing and guardrail rollouts alongside ChatGPT’s codebase, compressing the loop between research breakthroughs and shippable products. Raji is slated to run product engineering for ChatGPT and related systems, giving the new org both mandate and muscle.

This is also a signal on currency and timing. An all-stock purchase leverages OpenAI’s private paper while preserving cash for compute and custom silicon, and it lands amid a record M&A wave in A.I. CB Insights tracks quarterly A.I. deal counts at new highs in 2025, underscoring a land-grab for capabilities rather than customers.(source: CB Insights)

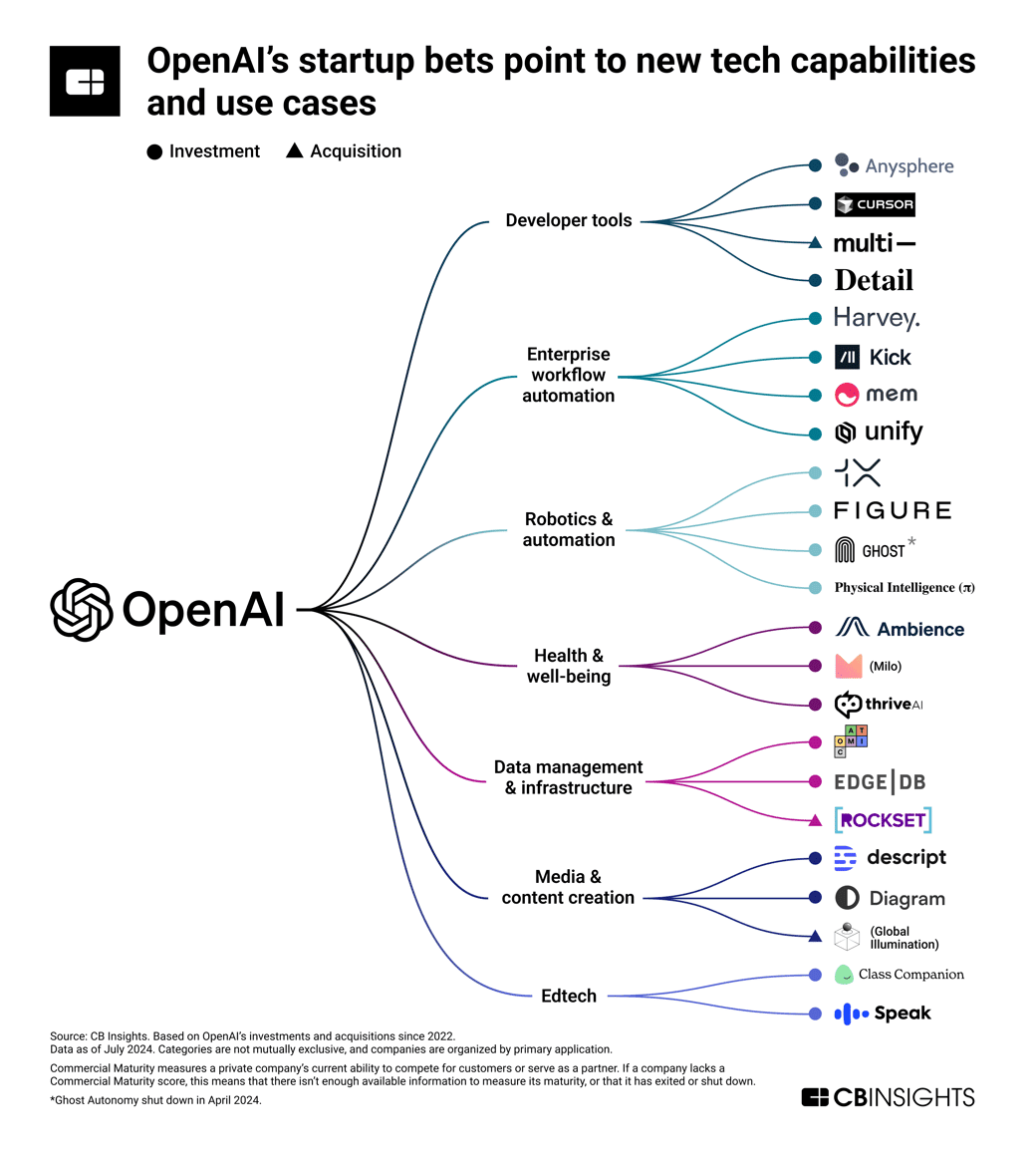

The applications stack, assembled

Look at OpenAI’s recent deal trail and a deliberate stack appears:

Design and UX — Global Illumination brought a product design team to reshape consumer surfaces.

Retrieval and data plumbing — Rockset added real-time indexing and hybrid search to ground models in fresh, enterprise-grade data. (source: Blocks and Files)

Collaboration surface — Multi’s team joined to fold multiplayer workflows and video-centric collaboration into ChatGPT’s work persona. (source: TechCrunch)

Evaluation — Context.ai’s founders arrived via acqui-hire, bolstering model analytics and eval pipelines that decide what is safe and shippable. (source: TechCrunch)

Personalisation — Crossing Minds’ recommender talent enhances ranking and suggestions, which are crucial for a product increasingly shaped by user history and intent. (source: TechCrunch)

Hardware — The io Products merger, led by Jony Ive, anchors a device pathway where on-device sensing and novel interfaces can differentiate latency, privacy and brand. Reported deal value: $6.5 billion. (source: Reuters)

Experimentation — Statsig closes the loop with experimentation and rollout control at scale.

Individually, these buys look tactical. Together, they form a vertically integrated applications engine: design → instrument → evaluate → retrieve → personalise → ship → iterate.

Power and org design

The creation of an Applications leadership layer under Simo professionalises what had been an increasingly sprawling product remit, and it rebalances influence away from pure research into shipping cadence, growth and safety operations. Raji’s remit across core systems and integrity gives the new org authority over the dials that govern real-world behaviour, from memory to moderation. That is where regulators, partners and large customers will focus next. (source: The Verge)

OpenAI’s internal economics also encourage this pivot. Reuters has reported a sharply rising revenue run-rate and ongoing secondary tender activity, the kind of pressure that rewards reliable application revenue and predictable upgrade cycles. Owning experimentation and evaluation makes revenue less lumpy and less dependent on headline model releases.

Competitive implications

For rivals, the message is blunt. Differentiation will hinge less on base model benchmarks and more on the speed and safety with which features move from idea to cohort to default. Google and Anthropic will need equivalent, tightly coupled experimentation and evaluation loops to avoid shipping more slowly and with less confidence in outcomes. The A.I. race is becoming an operations contest.

On the enterprise front, Rockset-backed retrieval, combined with Statsig-grade controls, positions OpenAI to court regulated buyers that insist on auditable rollouts and data residency. On the consumer side, Crossing Minds-style personalisation tied to device-level experience from io hints at a future where ChatGPT feels individually tuned across surfaces, not just another web app.

What to watch next

Bundling — Expect experimentation, evals and retrieval to surface as premium governance features in enterprise ChatGPT, priced as control, not compute.

Data policy — With experimentation and personalisation embedded, expect scrutiny of how user data flows across apps and devices; policy choices here will determine partner trust.

Org cadence — The real test for the Applications group will be cycle time: how often meaningful features ship and how safely they stick.

More programmatic M&A — CB Insights’ trendlines suggest the spree is not over; remaining gaps include billing/entitlements at scale and enterprise-grade observability for model-in-production.

Bottom line: Statsig is the keystone in an applications-first architecture. OpenAI is no longer just a model lab. It is building a product machine where experimentation, evaluation, and retrieval are native capabilities, not vendor integrations, and where power accrues to whoever can ship, learn, and iterate the fastest.