AI Investment and Unicorn Surge: Key Insights from Q3 2024

Despite a 29% drop in AI funding, deals hit record highs as generative AI startups thrive

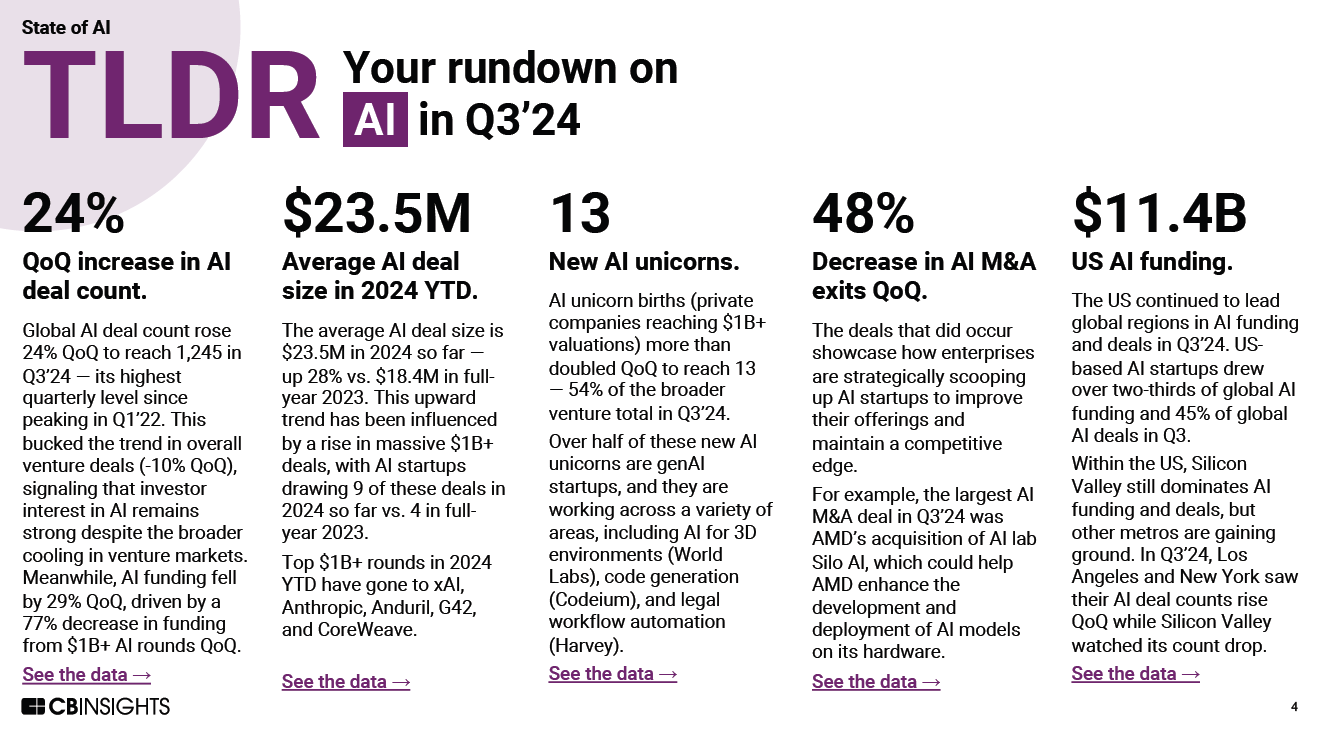

Q3 2024 witnessed a paradox in the AI sector: while overall funding decreased by 29%, the number of deals climbed to levels not seen since 2022. This trend underlines sustained investor interest in AI, particularly in generative AI (genAI), with 13 new AI unicorns emerging globally. The CB Insights report offers a detailed view of the evolving landscape of AI investments, deal sizes, geographic trends, and the dynamic rise of unicorns, even as broader venture markets cooled.

The Rise of AI Deals Amidst Reduced Funding

Although venture markets saw a general 10% decline, AI bucked this trend with a 24% quarter-over-quarter (QoQ) increase in deal counts, reaching 1,245 deals. However, funding did not follow suit; it decreased primarily due to a 77% reduction in $1 billion+ deals, indicating a shift toward smaller investments or earlier-stage funding.

This divergence suggests that investors are strategically supporting more diverse, smaller-scale startups. Many of these early investments target genAI applications in sectors as varied as 3D modelling, legal workflow automation, and code generation, appealing to markets beyond traditional tech giants.

New Unicorns and the Generative AI Boom

The third quarter also saw the birth of 13 new AI unicorns, making up over half of new venture unicorns in Q3 2024. The trend reflects an increased valuation for genAI-focused startups, such as Codeium, a code-generation platform, and World Labs, a company specializing in AI for 3D environments. This boom signals that genAI continues to attract interest from investors and companies looking to transform workflows, customer experiences, and productivity.

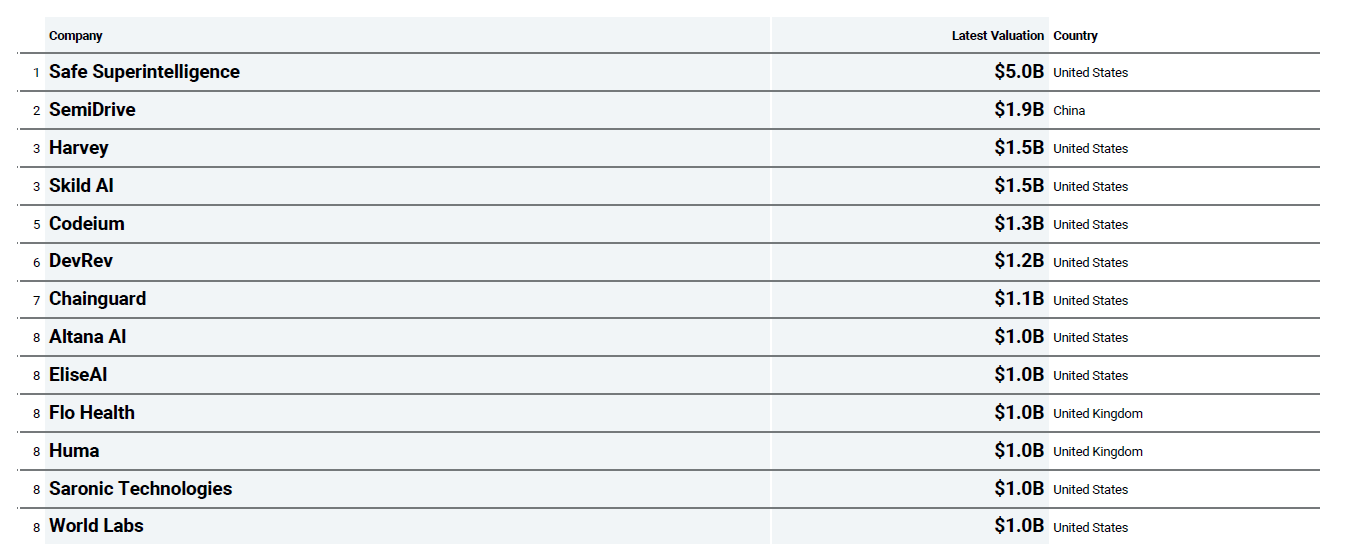

Figure: Global: Top unicorns by valuation in Q3’24 (CB Insights)

Among the standout new unicorns was Safe Superintelligence, valued at $5 billion, supported by Andreessen Horowitz and other top firms. Other notable names include Skild AI, a legal workflow automation tool valued at $1.5 billion, showing how even niche applications of AI are capturing significant attention and funding.

Figure: Global: Top unicorn births in Q3’24 (CB Insights)

Geographic and Deal Stage Trends

The report reveals that the United States remains the leader in AI funding and deals, capturing over two-thirds of global AI funding. However, deal distribution is beginning to even out as Europe and Asia invest heavily, particularly in generative and applied AI. Countries like China and India showed intense funding rounds in startups like Baichuan AI ($688 million) and ANSR ($170 million), underscoring a global shift in AI innovation beyond Silicon Valley.

Early-stage funding dominated, accounting for 72% of deals, while late-stage investments declined to just 6%. This early-stage focus may indicate investor confidence in the long-term potential of new AI entrants and applications, especially as companies are eager to establish footholds in emerging AI niches before they mature.

Why These Trends Matter to Business Leaders

For business leaders, these investment patterns highlight where competitive advantages will likely emerge. The focus on early-stage funding suggests that disruptive AI technologies are still in their infancy, offering opportunities for companies to integrate cutting-edge AI tools tailored to their industry needs. Additionally, the rise in smaller deal sizes allows more companies to access AI-powered solutions without requiring multi-billion-dollar budgets.

AI's potential in legal, healthcare, and industrial sectors has attracted particular interest. For example, Harvey’s legal workflow automation capabilities can streamline repetitive legal tasks, potentially reducing overhead costs. Similarly, AI's expansion into 3D modelling and environment creation could redefine visual media and e-commerce, as platforms such as World Labs enable more interactive digital experiences.

A Snapshot of Strategic AI Acquisitions

AI’s growing strategic value was also evident in mergers and acquisitions, such as AMD’s acquisition of Silo AI, which underscores AI’s importance in hardware-accelerated development. This acquisition and others reveal how established firms embed AI to drive differentiation and competitive advantage.

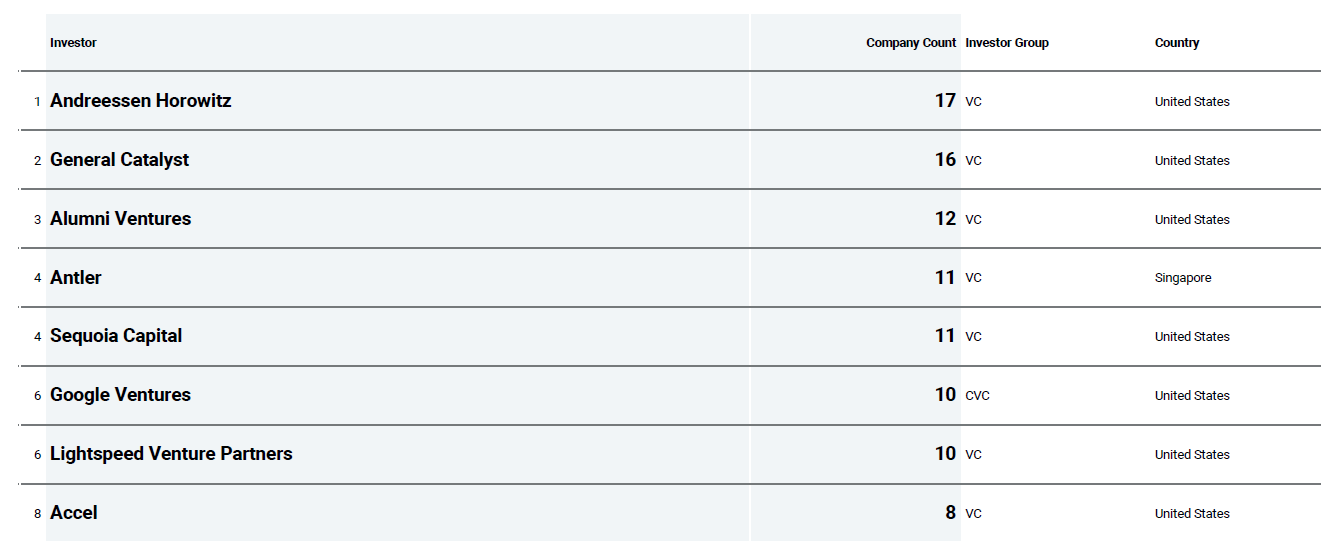

Figure: Global: Top investors by company count in Q3’24 (CB Insights)

Conclusion

The trends observed in Q3 2024 reveal a new era of strategic investments in AI. The emphasis on early-stage funding, the emergence of genAI unicorns, and the geographic spread of investments indicate that AI remains central to innovation agendas. For companies, AI represents both a tool for immediate operational gains and a longer-term path to market leadership through differentiation and enhanced capabilities.

As AI continues to evolve, business leaders who understand these shifts can position themselves to harness its power as a transformational force within their industries.